December 15, 2025 · The Couple Estates

30-Year Amortization for First-Time Home Buyers: A One-Year Retrospective on Canada's 2024 Mortgage Rule Changes

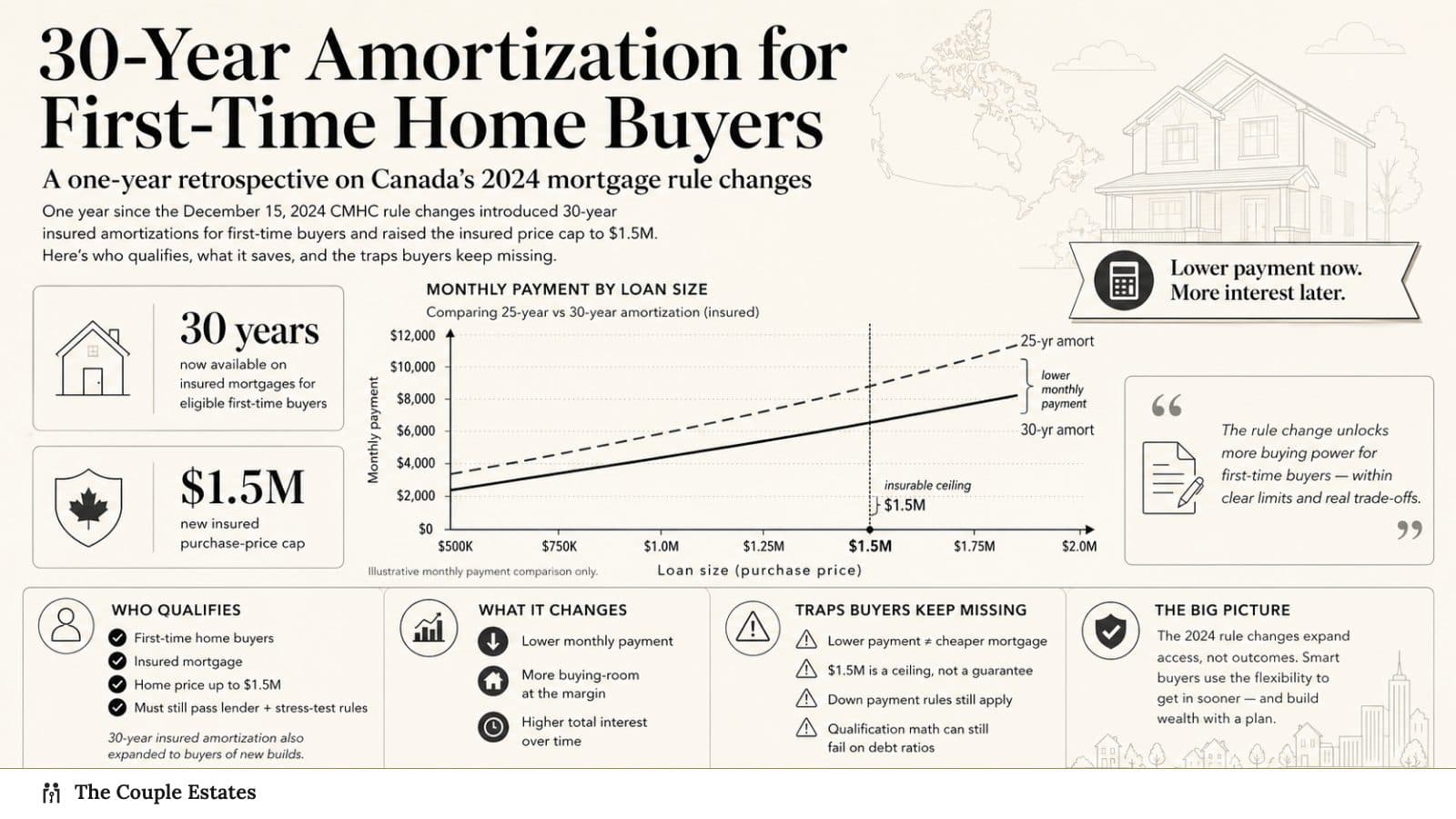

One year since the December 15, 2024 CMHC rule changes introduced 30-year insured amortizations for first-time buyers and a $1.5M insurable price cap. Here's who qualifies, what it saves, and the traps buyers keep missing.

It has been exactly one year since the biggest change to Canadian mortgage rules in a decade took effect. On December 15, 2024, CMHC rolled out two structural changes at once:

- 30-year amortization became available on insured mortgages for first-time home buyers and for any buyer of a new-construction home.

- The maximum insurable home price rose from $1 million to $1.5 million.

A year in, these rules are doing what they were designed to do — getting more first-time buyers approved in the GTA — but there are three traps that keep catching buyers by surprise. Here's what the rules actually say, what they save, and where people get tripped up.

The rules in plain English

30-year amortization (extended from 25)

If you are a first-time home buyer, you can get a 30-year amortization on an insured mortgage whether you buy new construction or resale.

If you are NOT a first-time home buyer, you can still get a 30-year amortization on an insured mortgage, but only if you are buying new construction (never previously lived in).

Uninsured mortgages (20%+ down payment) — the 30-year option has technically been available for a while. This change targets insured (under 20% down) buyers specifically.

$1.5M insurable price cap

Before the change, homes priced over $1M required a 20% minimum down payment — effectively excluding insured mortgages. Now:

- Insured mortgages available on homes up to $1.5M purchase price.

- Minimum down payment is 5% on the first $500,000 and 10% on the portion above $500,000 up to $1.5M.

- Down payment on a $1.5M home: 5% × $500K + 10% × $1M = $125,000.

This brought a huge chunk of GTA inventory — particularly detached homes in Mississauga, Brampton, Vaughan, and east-end Toronto — within reach of buyers who had between $75K and $150K saved.

What is a "first-time home buyer" for mortgage purposes?

The lender definition is slightly different from the CRA tax definition. For insured mortgage purposes, you are a first-time buyer if any one of these is true:

- You have never purchased a home before.

- You have not occupied a home as a principal residence that you or your spouse/common-law partner owned in the last 4 years.

- You recently experienced the breakdown of a marriage or common-law partnership.

Note the 4-year rule runs from the date of your mortgage application, not the calendar year like the CRA rebate.

What this saves you in actual dollars

Let's run a concrete example. A Brampton townhouse at $850,000, 10% down ($85,000), insured mortgage on the $765,000 balance at 4.29% fixed.

| Amortization | Monthly payment | Interest paid over 5-year term | Qualifying income needed |

|---|---|---|---|

| 25 years | $4,147 | $153,900 | ~$158,000 |

| 30 years | $3,757 | $157,200 | ~$144,000 |

| Monthly saving | $390 | — | — |

The 30-year amortization gets the buyer approved on a household income ~$14,000 lower than the 25-year equivalent. That is the real story of the change — not the monthly savings, but approval power.

Over the full life of the mortgage, the 30-year version does cost more in total interest (roughly $60,000 more if rates stayed constant, which they won't). But most buyers accelerate payments, refinance, or sell well before 30 years, so the lifetime cost differential is usually much smaller than the calculator suggests.

Trap #1: Assuming 30-year is automatic on any insured mortgage

It's not. Many buyers walk into a bank branch assuming 30-year amortization is the default for insured mortgages. It's not. You have to specifically qualify as a first-time buyer (for resale) or have the property qualify as new construction (for non-FTHB).

Banks will often offer 30-year without asking. But if you're a non-FTHB buying resale and the lender sets you up on a 30-year insured, expect the CMHC application to get rejected or re-priced. Confirm the amortization in writing with your mortgage broker or lender before your offer goes firm.

Trap #2: Confusing "new construction" definitions

For the 30-year amortization to apply under the new-construction path, the home must be:

- Newly built and never previously occupied, OR

- Have undergone substantial renovation (effectively replacing most of the interior).

What does NOT qualify:

- A resale home built in 2023 that has had owners.

- An assignment purchase where the original buyer occupied it.

- A condo that the builder rented out before selling.

- A "renovated" home where the owner did some kitchen and bathroom work.

If your deal is on any of these, the 30-year path is not available unless you're a first-time buyer qualifying via the FTHB route.

Trap #3: The $1.5M cap is hard-line

The insured mortgage ceiling is $1.5M — full stop. A $1,501,000 purchase price takes you out of the insured market entirely. This is the one cliff in the system — there's no graduated phase-out, no partial insurance.

Buyers bidding in competitive situations sometimes end up at a final offer price of $1.51M or $1.52M on a property they were planning to buy with 10% down. That pushes the deal into uninsured territory, which requires 20% down — suddenly $300,000 instead of $140,000 in cash.

Watch your bidding ceiling. If you're using an insured mortgage, do not stretch past $1.5M on price, even if you think the house is worth it.

How this interacts with other programs

Stacking opportunities:

- Home Buyers' Plan: Withdraw up to $60,000 (or $120,000 per couple) tax-free from RRSPs toward your down payment. Must be repaid over 15 years starting the second year after withdrawal.

- First Home Savings Account: Contribute up to $8,000/year with a $40,000 lifetime cap. Contributions are tax-deductible, withdrawals for a qualifying first home are tax-free. Best combined with an HBP withdrawal.

- Ontario & Toronto LTT first-time buyer rebates: Up to $4,000 provincially, plus up to $4,475 in Toronto, rebated at closing.

- FTHB GST/HST Rebate (new construction only): Up to $50,000 federal + up to $80,000 provincial = up to $130,000 on qualifying new builds. Our full guide here.

For a first-time buyer purchasing a $950,000 new-build in the GTA, the stack of programs available at closing looks like:

- HBP withdrawal (tax-free): up to $60,000

- FHSA contribution (tax-deductible): up to $40,000

- HST rebate on new build: up to $123,500 (federal + provincial combined, phased at this price)

- Ontario LTT rebate: $4,000

- Toronto MLTT rebate (if in Toronto): up to $4,475

- 30-year insured amortization: ~$390/month savings vs 25-year

It is the most generous package for first-time GTA new-build buyers in at least 15 years. The catch: you have to know the programs exist and apply them correctly.

Looking ahead

Industry has been asking the federal government to extend 30-year amortization to all insured resale mortgages, not just first-time buyers. Budget 2025 (tabled November 4) did not include that extension. It remains a possibility in future budgets but is not currently on offer.

Similarly, there has been pressure to raise the $1.5M insurable cap to $2M — also not in Budget 2025. For now, $1.5M is the ceiling.

If you're thinking about a first-time purchase in 2026 and want to walk through what the combined mortgage rules, rebates, and new-build incentives would look like on a specific price range, get in touch — happy to run your personalized stack.

Sources

- CMHC — Mortgage Rules 2026 (overview)

- CMHC — Revises Homeowner Mortgage Loan Insurance Premiums

- Department of Finance Canada — 30-year amortization expansion

- TD Economics — Mortgage Rule Changes to Add Fuel to Canadian Housing Recovery

- Level Up Mortgages — Impact of 30-year amortization for first-time buyers