March 25, 2026 · The Couple Estates

Pre-Construction Condo Investing in the GTA 2026: True Cost After HST, Assignments, and Closing

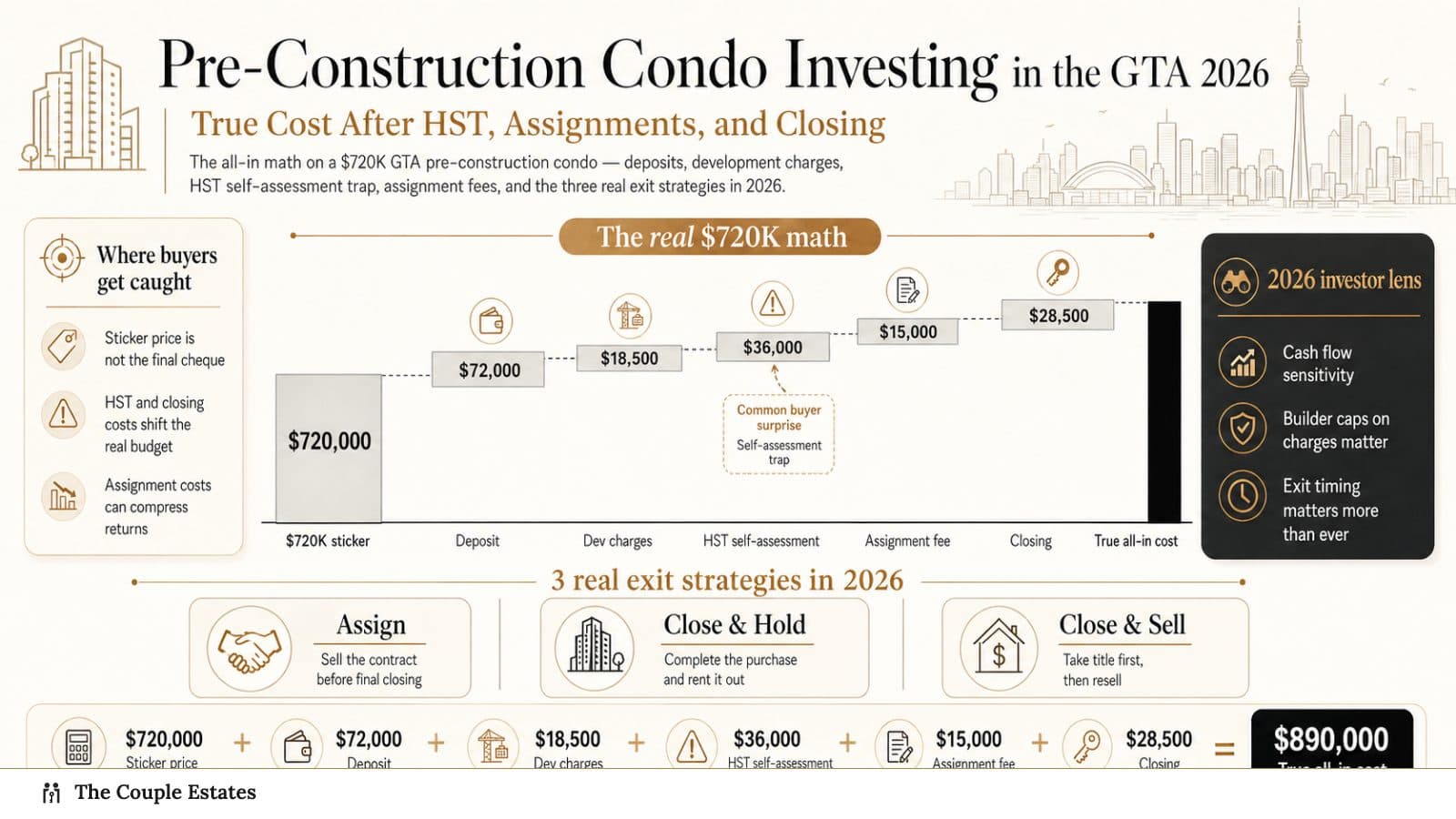

The all-in math on a $720K GTA pre-construction condo — deposits, development charges, HST self-assessment trap, assignment fees, and the three real exit strategies in 2026.

Builder brochures lie about returns. Not by misstating any single number — the per-square-foot price on the floorplan sheet is real, the projected rent is in the right ballpark, the "5% projected yield" calculation isn't fabricated. They lie by omission. The $720,000 sticker price on a 1+den in a Mississauga pre-construction tower is not the price you actually pay to take possession four years later. By the time you close, you will have wired the builder roughly $144,000 in deposits, paid 6–18 months of interim occupancy carry, absorbed $45K–$75K in closing-day adjustments, and either settled or fought the HST self-assessment trap. The brochure's "yield" math ignores all of it.

This is the all-in math on a representative $720,000 GTA pre-construction 1+den in 2026 — what you actually pay, when you pay it, what the CRA expects from you the day you take possession, and the three exit strategies that are still defensible at this point in the cycle. No fabricated project names, no boosterism, no "appreciation will solve it" hand-waves. The numbers below are what the deal actually looks like.

The deposit ladder + interim occupancy carry

Builder deposit structures in the GTA in 2026 are remarkably consistent. The standard deposit ladder on a $720,000 unit is 20% over roughly 24 months, paid in five tranches:

| Milestone | Timing | % | $ on $720K |

|---|---|---|---|

| With offer | Day 0 | 5% | $36,000 |

| 30 days | Day 30 | 5% | $36,000 |

| 90 days | Day 90 | 5% | $36,000 |

| 365 days | Day 365 | 5% | $36,000 |

| Occupancy | Day 700–900 | (rolled in) | — |

| Total deposit | 20% | $144,000 |

The first $36,000 cheque clears your bank within 24 hours of signing. There is a 10-day rescission window in Ontario under the Condominium Act — that's your only opportunity to walk away without consequence. After day 10, the deposit is at risk, and pulling out costs you the full ladder plus damages.

What the brochure does not show: the interim occupancy carry. Most GTA pre-con units are ready to occupy 6–18 months before the condominium corporation is registered with the Land Registry Office. During that window, the buyer takes physical possession but does not yet hold title — and instead of paying a mortgage, the buyer pays the builder a monthly occupancy fee that combines three components: estimated mortgage interest on the unpaid balance, estimated property taxes, and estimated common-element fees.

On a $720,000 unit with a $576,000 unpaid balance, typical 2026 interim occupancy carry is $2,650–$2,950 per month for the full 6–18 months. None of that money builds equity — the principal isn't being paid down because there isn't a registered mortgage yet. Across a 12-month interim occupancy window, that's roughly $33,600 paid to the builder for the privilege of living in your own unit while you wait for registration.

The real out-of-pocket position on a $720K pre-con before closing day is $144K in deposits plus $20K–$50K in interim occupancy fees, none of which builds equity. That is the number to put on the spreadsheet, not the brochure's "20% down" line.

Closing-day adjustments — the surprise line items

The day the building registers and your unit closes is also the day the builder's lawyer hands your lawyer the statement of adjustments — a multi-page invoice of extras that the agreement of purchase and sale (APS) authorized but did not quantify at the time you signed. The categories are predictable. The dollar values are not, because most are written into the APS as "to be determined" or "not to exceed" caps that the builder sets close to the cap.

| Adjustment | Toronto (416) | Mississauga (L5) | Vaughan (L4 / L6) |

|---|---|---|---|

| Municipal development charges | $35,000–$55,000 | $25,000–$38,000 | $28,000–$42,000 |

| Education levy (school board) | $1,800–$3,200 | $1,800–$3,200 | $1,800–$3,200 |

| Parkland / parks levy | $2,500–$8,000 | $2,500–$5,500 | $2,500–$5,500 |

| Tarion enrolment fee | ~$1,800 | ~$1,800 | ~$1,800 |

| Utility hookups (hydro, water, gas) | $2,200–$3,000 | $2,200–$3,000 | $2,200–$3,000 |

| Law Society levy + Teraview | $200–$400 | $200–$400 | $200–$400 |

| HST adjustment (if assigned) | varies | varies | varies |

| Typical total on $720K unit | $50,000–$75,000 | $38,000–$58,000 | $42,000–$62,000 |

A few line items deserve a closer look. Municipal development charges are the largest and most variable: City of Toronto's residential DC schedule is materially higher than Mississauga's or Vaughan's, and the City of Toronto reserves the right to increase DCs between APS signing and closing — your APS almost certainly includes a clause passing that increase through to you. Builders cap the pass-through (typical caps run $15,000–$25,000), but the cap is the cap, not a refund — they will charge to the cap if the city raised DCs at all.

The Tarion enrolment fee funds the Ontario new-home warranty backstop under the ONHWPA. It's mandatory, not negotiable, and it's the seller-payable side of the warranty coverage you'll rely on if there are deficiencies after possession.

The HST adjustment line only matters on assigned units, and it is the source of the most expensive surprises in the entire pre-con space — covered in the next section.

Plan for $45K–$75K of closing-day cash on a $720K Mississauga unit, on top of the $144K already in deposits. That is the second column of the spreadsheet the brochure didn't show you.

The HST self-assessment trap

This is the single most expensive misunderstanding in GTA pre-construction investing, and it catches sophisticated buyers every cycle. The mechanics:

The builder's posted price (the $720,000 on the brochure) is HST-inclusive, but only on the assumption that the end buyer will live in the unit as a primary or secondary residence. Under that assumption, the builder applies the HST New Housing Rebate on the buyer's behalf at closing — roughly $24,000 of federal + Ontario rebate combined on a $720,000 unit — and adjusts the contract price downward by the rebate amount. The buyer signs at $720K and effectively pays the builder the rebated net.

If the buyer is an investor — i.e. the unit will be rented to a tenant on closing rather than occupied by the buyer or a family member as a principal residence — the New Housing Rebate does not apply. The CRA's position is unambiguous: the rebate is for owner-occupants. Rental investors must:

- Repay the New Housing Rebate to the builder at closing. The builder's lawyer will ask the buyer's lawyer to confirm intent. If the buyer cannot sign a statutory declaration of intent to occupy, the ~$24,000 gets added to the closing adjustments. This is the line item most investors don't know is coming.

- File for the New Residential Rental Property Rebate (NRRPR) via CRA Form GST524 within 2 years of substantial completion. The NRRPR is functionally equivalent to the New Housing Rebate (~$24,000 on a $720K unit) but is paid directly to the buyer by CRA after the rental is in place and a 1-year tenancy has been documented.

The trap has two failure modes. The first is investors who claim end-user intent at closing to avoid paying the $24K, then rent the unit anyway — the CRA reassesses regularly and recovers the rebate plus penalty plus interest, and the reassessment window is six years. The second is investors who correctly repay at closing but never file the NRRPR — the rebate they are entitled to evaporates after the 2-year deadline, and that is $24,000 of permanent loss.

| Scenario | At closing | Within 2 years | Net HST cost |

|---|---|---|---|

| End-user buyer | Builder credits ~$24K rebate | No filing required | $0 net |

| Investor — handles correctly | Repay ~$24K to builder | File NRRPR via GST524, recover ~$24K | $0 net |

| Investor — claims end-user, gets reassessed | Saves $24K at closing | CRA recovers $24K + penalty + interest | $28K–$32K net (worse than honest path) |

| Investor — repays at closing, forgets to file | Pays ~$24K | NRRPR window closes | $24K net loss |

Investors must repay the New Housing Rebate at closing and then claim the NRRPR via CRA Form GST524 within 2 years of substantial completion — there is no shortcut, and the cost of getting this wrong is $24K–$32K per unit. The CRA's RC4231 guide is the source document; do not rely on the builder's lawyer to walk you through it, because their client is the builder, not you.

Assignment economics

The assignment market is the pre-con space's pressure valve — investors who can't or won't close at delivery sell their APS rights to a third party before registration. Most builders permit assignments under restrictive conditions: only after the contract goes firm (post-rescission and typically after the second or third deposit milestone), with the builder's prior written consent, and on payment of a consent fee. The fee schedule on a 2026 GTA pre-con APS typically runs:

| Friction line | Cost on a $720K APS assigned at $755K |

|---|---|

| Builder consent fee | $5,000–$25,000 |

| Assignor's lawyer | $1,500–$3,000 |

| Real estate commission (if listed) | $0–$15,000 |

| HST on assignment profit | ~$4,500 (13% of $35K markup) |

| Capital gains on profit (50% inclusion at top marginal rate) | ~$8,400 |

| Builder admin / occupancy adjustments | $1,500–$3,000 |

| Total friction | $20,900–$58,900 |

The worked example: a $720,000 APS signed in 2024, assigned in 2026 at $755,000 — a $35,000 gross markup. After a mid-range $35,000 of friction (builder consent on the high end, lawyer, commission to a listing agent, HST on the profit, capital gains), the assignor nets roughly zero to $5,000. On the low-friction end with a permissive builder and a private buyer, net might reach $10,000–$15,000. On the high-friction end with a restrictive builder and a brokered sale, net is genuinely negative.

That math is why most assignments only work in strong appreciation windows. A $720K APS assigned at $820K (a $100K markup) clears $40K–$60K net after friction — workable. A $720K APS assigned at $750K (a $30K markup) is a money-losing exercise once you net the friction, and the assignor would have been better off closing and pursuing a different exit.

Assignments are a viable strategy only when the markup-to-friction ratio is at least 2:1 — meaning a minimum $50K markup on a $720K APS to net any meaningful return. In flat or softening markets, the assignment market dries up because the math stops working, which is exactly when investors most want to exit.

Three real exit strategies

After the deposits, the closing adjustments, the HST resolution, and the assignment math, the question reduces to: what do you actually do with the unit? Three strategies are defensible in 2026; the others (short-term rental, flip-on-close-no-occupancy) are either regulated out of existence in most GTA municipalities or carry tax treatments that destroy the math.

Strategy 1 — Hold-to-tenant (cap rate ~3.4% gross, appreciation play)

The default investor exit. Take possession on closing, place a tenant, hold for 5–7 years, sell into an appreciated market.

The 2026 cap rate math on a representative $720K Mississauga 1+den, rented at $2,650/month:

- Gross annual rent: $31,800

- Operating costs (condo fees ~$680/mo, property tax ~$310/mo, insurance ~$45/mo, vacancy/repairs allowance ~$80/mo): ~$13,380/year

- Net operating income: ~$18,420/year

- Gross cap rate: 31,800 / 720,000 = 4.4%

- Net cap rate (NOI / purchase price): 18,420 / 720,000 = 2.6%

At any reasonable leverage (say, 65% LTV at a 4.5% mortgage rate), the unit is cash-flow negative by $400–$700/month after debt service. The investor is funding monthly losses out of personal income and betting on appreciation to recover the carry plus generate a return.

Honest tradeoff: this strategy works if you have a 5–7 year horizon, sufficient personal cash flow to cover the monthly negative carry, and a thesis on why this submarket will appreciate above the 5-year baseline. It does not work as a passive income strategy, full stop — there is no passive income at 2026 cap rates in the GTA.

Strategy 2 — Assignment in pre-firm window (rare, high friction, only in strong markets)

Cover the deposit ladder, monitor the resale market for 18–24 months, list the assignment when (and only when) the local resale comp set has appreciated enough to clear $50K+ over your APS price after all friction.

The window for this strategy is narrow. It only works in markets that appreciated sharply between APS signing and assignment — and 2024–25 in the GTA was not such a market. Through most of the post-2022 reset, assignment prices have run at or below APS prices, meaning assignors have sold at a loss simply to escape the closing obligation. The few profitable assignments in the cycle have been in master-planned 905 communities with thin resale supply or in 416 sub-pockets with unique transit catchment.

Honest tradeoff: assignment as a planned strategy is timing-dependent and outside the assignor's control. Treat it as an option, not a plan.

Strategy 3 — End-user occupancy then sell at year 2 (best tax outcome, principal residence exemption)

Take possession, move in, designate the unit as your principal residence for tax purposes, live there for at least 12 months (CRA's "ordinarily inhabited" threshold), then sell. Any capital gain is shielded by the principal residence exemption (PRE), which is the cleanest tax outcome available on a pre-con investment.

The mechanics:

- HST: end-user, builder credits the rebate at closing, no NRRPR exposure

- Capital gains: zero on sale, fully shielded by PRE for the years the unit was your principal residence

- 4-year capital lock-up: yes — the deposits, closing costs, and 1–2 years of mortgage payments are all tied up in the unit and cannot be redeployed elsewhere

The tradeoff is opportunity cost. The investor has roughly $200K of capital tied up (deposits + closing extras + initial principal paydown) for 3–4 years before the sale clears, during which time that capital is not earning any other return. The compensating advantage is that the gain — assuming any appreciation — is entirely tax-free, where the same gain on a rental hold would be taxed at ~25% effective (50% inclusion at top marginal rate).

End-user occupancy followed by a year-2 sale is the cleanest 2026 pre-con strategy on tax grounds, provided the investor can absorb the 4-year capital lock-up. It is the only one of the three exits that does not depend on either negative cash flow being recovered later or a strong appreciation window arriving on schedule.

Linked reading

For the rental cap rate math at scale across GTA submarkets, see GTA rental cap rates 2026. For the buyer-side mortgage context that determines who is likely to buy your unit at exit, see 30-year amortization for first-time home buyers.

If you are weighing a specific pre-con allocation against alternatives — resale condo, GTA detached, or a non-real-estate deployment — the deposit ladder, closing adjustments, and HST resolution all need to be in the same spreadsheet before the comparison is honest. Most pre-con pitches are not built that way.

Sources

- CRA — RC4231 GST/HST New Housing Rebate guide

- CRA — Form GST524 New Residential Rental Property Rebate Application

- Tarion — New Home Warranty enrolment fee schedule

- City of Toronto — Development Charges By-law and rate schedule

- City of Mississauga — Development Charges By-law

- Ontario New Home Warranties Plan Act (ONHWPA), R.S.O. 1990, c. O.31

- Government of Ontario — Condominium Act, 1998 (10-day rescission)

Frequently asked questions

Investors do — and they have to self-assess. The builder typically credits the HST New Housing Rebate at closing assuming the buyer will live in the unit. If you rent it instead, you must repay the rebate (~$24K on a $720K unit) and apply for the New Residential Rental Property Rebate via CRA.

Builder consent fees for an assignment run $5,000–$25,000, plus your lawyer ($1,500–$3,000), plus HST on the assignment profit, plus capital gains. Total friction often hits $40,000–$60,000 before you net any markup, which is why most assignments only make sense in strong appreciation windows.

Most builders allow assignments only after the contract goes firm (post-rescission, post-deposit milestones), and they charge consent fees plus require board / counsel approval. Some restrict assignments entirely until interim occupancy. Check Schedule A of your APS before signing.

Only with a 5–7 year horizon and clear appreciation thesis. Cap rates at delivery are typically 3.0–3.5% gross — negative cash flow at any reasonable leverage. End-user occupancy followed by sale at year 2 is the cleanest tax outcome and the most defensible 2026 strategy.