March 18, 2026 · The Couple Estates

Bank of Canada Holds at 2.25% — Again. What the March 2026 Rate Decision Means for Ontario Buyers, Sellers, and Renewers

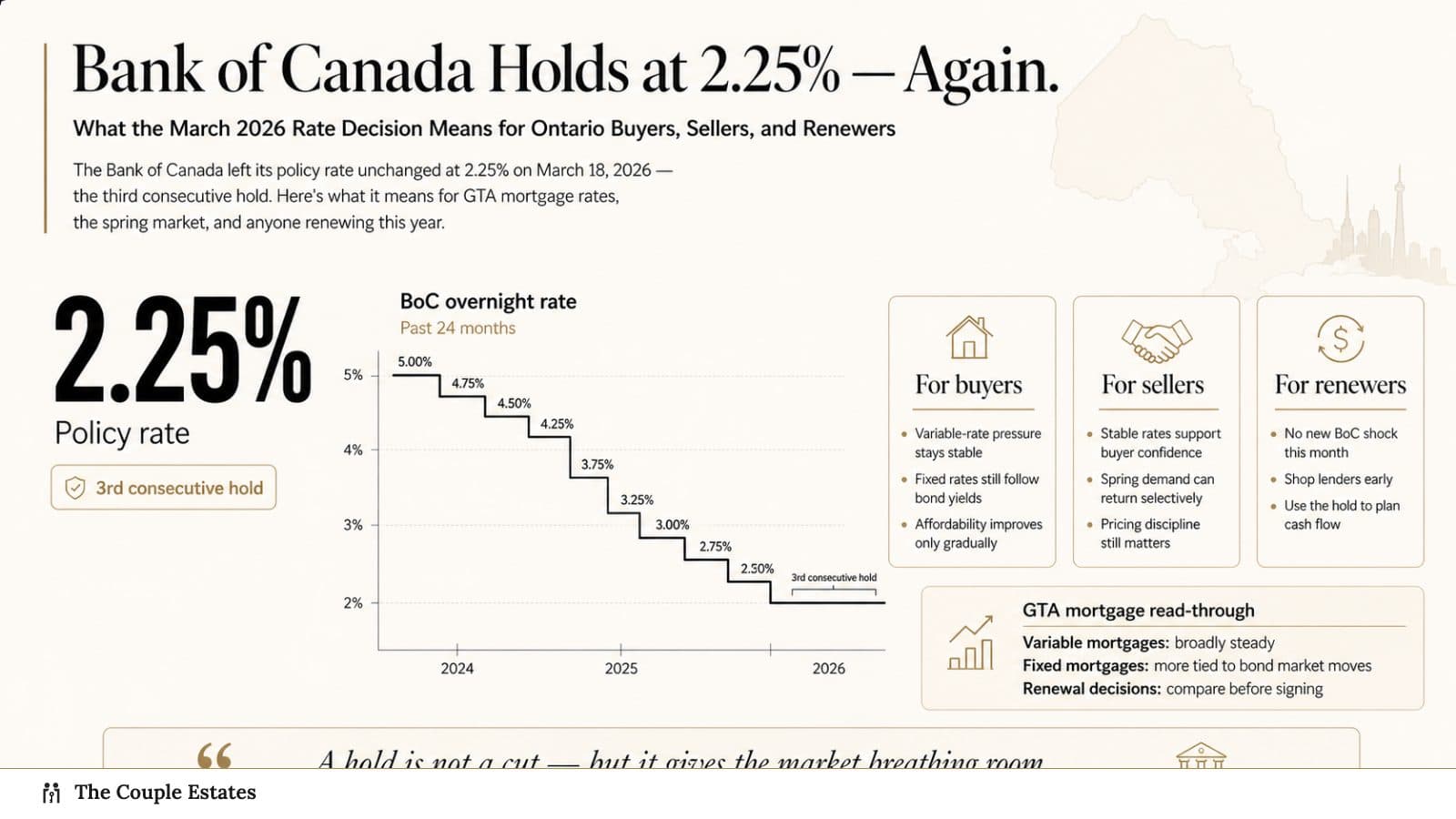

The Bank of Canada left its policy rate unchanged at 2.25% on March 18, 2026 — the third consecutive hold. Here's what it means for GTA mortgage rates, the spring market, and anyone renewing this year.

The Bank of Canada held its policy rate at 2.25% this morning — the third consecutive hold, and the longest pause since the tightening cycle of 2022–2023.

If you were hoping for a March cut to lean into spring, today's decision is a reminder that the Bank is not done worrying about inflation yet. But the statement is more dovish than January's, and the door to further cuts later in 2026 is clearly open. Here's the breakdown, and what it means if you're shopping, selling, or renewing in the GTA right now.

The bottom line

- Overnight rate: held at 2.25%. Bank Rate 2.5%, deposit rate 2.20%.

- Inflation: CPI fell to 1.8% in February, down from 2.3% in January. Core measures also near 2%.

- Growth: weaker than the January MPR projected — US tariffs are the main drag.

- Labour market: unemployment ticked up to 6.7% in February; Q4 2025 job gains have reversed.

- New wildcard: the war in Iran has pushed global energy prices up. The Bank expects gasoline to lift headline inflation over the next few months.

- Next decision: April 29, 2026, with an updated Monetary Policy Report.

The Bank of Canada's overnight rate, showing the October 2025 cut to 2.25% and the three subsequent holds through March 2026. Source: Bank of Canada.

The Bank of Canada's overnight rate, showing the October 2025 cut to 2.25% and the three subsequent holds through March 2026. Source: Bank of Canada.

What the Bank actually said

Governor Tiff Macklem's statement was a study in patience. The Bank's case for holding — after cutting 225 basis points from the 4.50% peak in 2024–2025 — comes down to three things:

- Inflation is right where they want it. Total CPI at 1.8% is already below the 2% target. Core measures are hovering at 2%. There is no inflation emergency to fight.

- But energy prices just jumped. The conflict in Iran has pushed crude higher. Gasoline flows through to CPI within weeks, so the Bank expects headline inflation to drift up from here — even if underlying pressure keeps easing.

- Growth is soft but not in freefall. Q4 2025 jobs gains reversed in January and February. Unemployment is at 6.7%. US tariffs continue to bleed into Canadian exports. The Bank wants to see whether this softness deepens before adding more stimulus.

Translation: we are not cutting today, but if growth keeps weakening and oil settles down, we have room to cut later.

What it means for mortgage rates

Variable-rate mortgages are priced off the prime rate, which sits at 4.45% at most major Canadian lenders today (prime = BoC overnight + 2.20%). With the Bank on hold, variable rates do not move. Full stop.

Fixed-rate mortgages move with Government of Canada bond yields, not directly with the BoC decision. The 5-year GoC bond has drifted between 2.85% and 3.10% over the past month, so best-in-market 5-year insured fixed rates are hovering in the 4.19% to 4.39% range. Uninsured conventional fixed rates are a shade higher, typically 4.39% to 4.59%.

What shifts after today's statement:

- If oil prices keep climbing and headline inflation surprises to the upside, bond yields push up, and fixed rates rise 10–20 bps in the next two to four weeks.

- If US tariff news worsens and jobs numbers stay weak, yields fall, and fixed rates drift toward 3.99% by early summer. This is still the more likely path based on today's tone.

For most buyers, the practical takeaway is simple: rates are not going meaningfully higher from here, and they are probably going lower by Q3 — but the size of any further cuts is smaller than last year's cycle.

What it means for the GTA spring market

The spring market opened weak. TRREB's February data showed GTA sales down 6.3% year-over-year and the average price at $1,008,968, off 7.1% from a year ago. A March rate cut would have given buyer psychology a clear signal to lean in. Instead, the market stays in the same tug-of-war it has been in since November:

- Inventory is elevated. Active listings are running above the 10-year average across most GTA sub-markets — especially condos.

- Prices have reset. The MLS HPI composite benchmark is down roughly 8% YoY. A lot of buyers who stayed out for three years now see homes they can actually afford.

- But affordability still hurts. Even at 4.2% fixed, a $900K mortgage runs $4,800/month on a 30-year insured amortization. Wage growth has not kept up.

The sellers who are realistic on price are getting sold. The sellers still anchored to 2022 comps are sitting. That split is unlikely to change without either a material rate cut or a demand shock.

If you've been waiting for "the bottom," the data says you're close — but don't expect a starter pistol. The cleanest windows to buy this cycle are likely to look, in hindsight, like the last four weeks rather than anything dramatic.

Browse current GTA listings or set up a saved search so you see new inventory the moment it hits.

What it means if you're renewing in 2026

Roughly 1.2 million Canadian mortgages are coming up for renewal in 2026, most of them signed in 2020–2021 at rates under 2%. Renewal shock is real — a household renewing from a 1.89% five-year fixed onto a 4.29% five-year fixed on a $600K balance will see payments rise from roughly $2,500 to $3,260 per month.

Three things to do right now if you're in that cohort:

- Shop six months early. Most lenders hold rates for 120 days. You can lock a rate today for a renewal as late as July.

- Don't auto-renew. Your existing lender's renewal offer is almost always 40–70 bps higher than what a broker can negotiate elsewhere. Under OSFI's updated rules, uninsured straight-switch renewals no longer require the stress test, so moving lenders is materially easier than it used to be.

- Consider a shorter term. A 2- or 3-year fixed in the 4.0% range lets you renew again closer to what most economists expect to be a lower-rate environment in 2027–2028 without gambling on a variable.

What to watch next

- April 16: February CPI release from Statistics Canada — the number that will dominate the April decision.

- April 29: Next BoC decision, with a fresh Monetary Policy Report. This is the meeting the market is pricing a 40% probability of a 25-bp cut.

- Ongoing: US tariff policy and Iran oil flows. Both are genuine wildcards.

The Bank is in patience mode. Buyers and sellers should be, too — but not paralysis mode. The fundamentals that matter to a specific home on a specific street (price, days on market, comparables within three doors) are where your attention belongs.

Questions about how today's decision affects your specific mortgage or purchase timing? Reach out — happy to run the numbers.

Sources

- Bank of Canada — Policy rate announcement, March 18, 2026

- Bank of Canada — Opening statement, March 18, 2026

- TRREB — GTA February 2026 market watch

- OSFI — Minimum qualifying rate for uninsured mortgages