April 29, 2026 · The Couple Estates

Bank of Canada Holds at 2.25% — April 29, 2026 Rate Decision Recap

The Bank held the overnight rate at 2.25% on April 29, 2026, looking through an energy-led inflation bump. Here's what it means for GTA mortgages, buyers, and renewers.

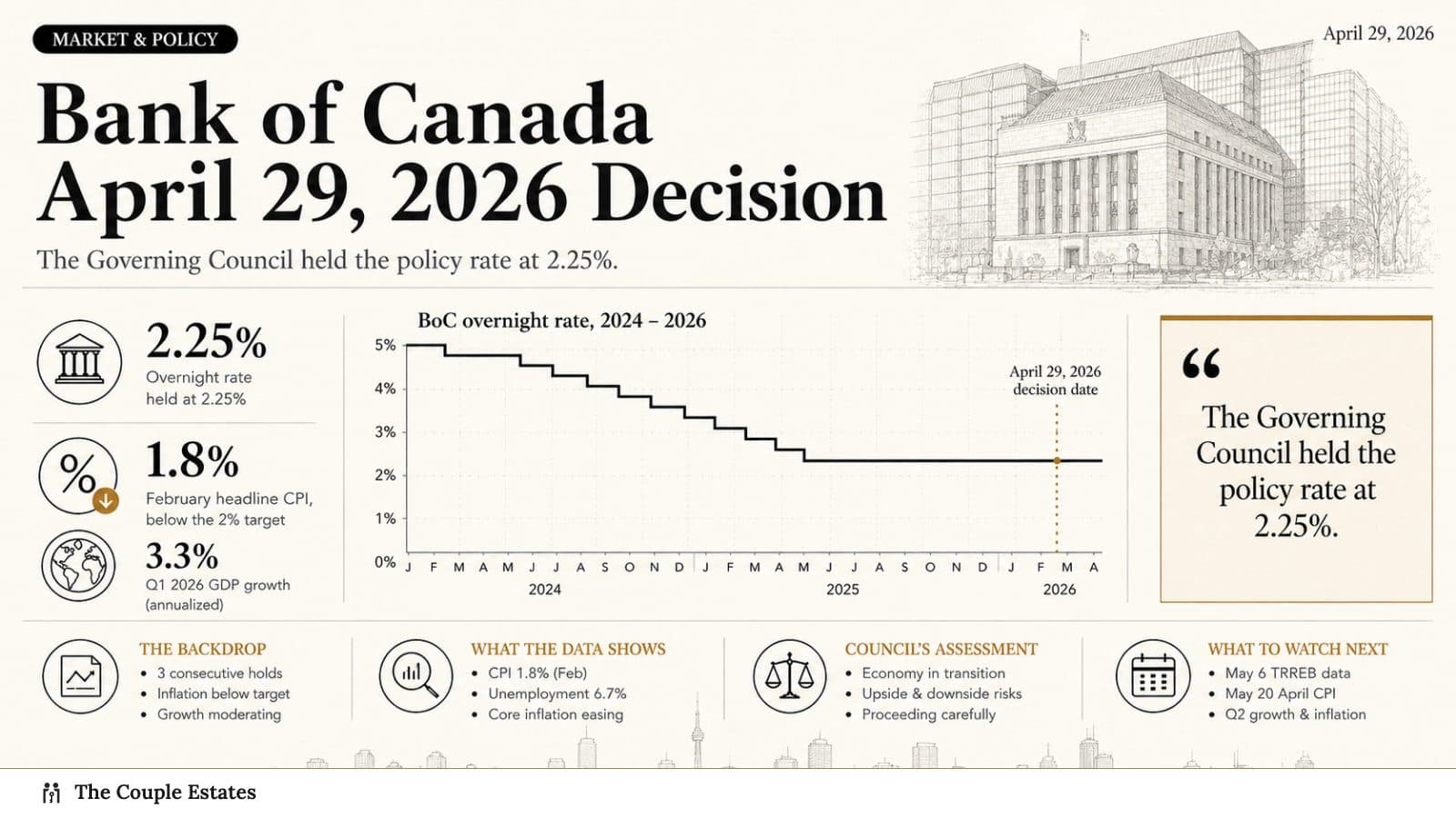

The Bank of Canada held its target for the overnight rate at 2.25% this morning — the fourth consecutive hold, and the longest pause since the 2022–2023 tightening cycle. The Bank Rate stays at 2.5%, the deposit rate at 2.20%.

This was the call our April 29 preview walked through under "Scenario A": a hold, with the Governing Council deliberately looking through an energy-driven inflation bump while keeping the door open to cuts later this year. What follows is what the statement actually said, what changed in the updated Monetary Policy Report, and how each piece lands for someone buying, selling, or renewing in the GTA right now.

The bottom line

- Policy rate: held at 2.25%. Bank Rate 2.5%, deposit rate 2.20%. Six consecutive months at this level.

- Inflation: March CPI climbed to 2.4% on a gasoline spike; the Bank expects April near 3%. Core inflation held just above 2%, and longer-term inflation expectations remain anchored.

- Growth: the MPR projects real GDP at 1.2% in 2026, rising to 1.6% in 2027 and 1.7% in 2028 — little changed from January, with a Q4 2025 contraction now in the rear-view.

- Labour market: unemployment in the 6.5%–7% range, with job losses concentrated in sectors targeted by US tariffs.

- Forward guidance: Governing Council is "looking through the war's immediate impact on inflation but will not let higher energy prices become persistent inflation."

- Next decision: June 4, 2026.

What the Bank actually said

Governor Tiff Macklem's statement was a study in selective patience. The case for holding — after 225 basis points of cuts from the 2024 peak — comes down to three judgements made simultaneously:

- The energy shock is real, but the Bank thinks it's temporary. The April outlook assumes Brent crude declines to US$75 per barrel by mid-2027. On that path, headline inflation peaks near 3% in April, then drifts back to the 2% target early in 2027.

- Underlying inflation is still close to target. Core measures held just above 2% in the most recent data, the share of CPI components running above 3% has been falling, and longer-term inflation expectations are anchored. There is, as the Bank put it, "little evidence that oil prices have fed through more broadly to goods and services prices" — a status the Bank flagged as something it will watch closely.

- Domestic demand is soft, not collapsing. Q4 2025 contracted, growth resumed in early 2026, and the unemployment rate sits in the 6½–7% range — soft enough to argue against tightening, not weak enough to demand stimulus on top of a price shock.

Macklem framed the decision plainly:

"Governing Council is looking through the war's immediate impact on inflation but will not let higher energy prices become persistent inflation. As the outlook evolves, we stand ready to respond as needed. The Bank is committed to maintaining Canadians' confidence in price stability through this period of global upheaval."

That is the operating word in this cycle: looking through. It buys the Bank time. It also explicitly conditions the next move on whether Iran-driven energy prices stay contained to gasoline — or start showing up in airfares, freight, food packaging, and services.

What changed since the March 18 hold

Three things have moved in six weeks. The picture is genuinely mixed:

1. March CPI confirmed the energy bump. Headline inflation jumped from 1.8% in February to 2.4% in March, almost entirely on gasoline. Core trim and median measures stayed clustered just above 2%. The disinflation story is intact under the surface; the headline number is now temporarily above target.

2. Iran's effect on global financial conditions has settled into a pattern. Bond yields are modestly higher than January. Equities, which sold off sharply at the start of the war, have round-tripped. The US dollar has appreciated against most majors, but the Canada–US exchange rate has been "relatively stable" — a meaningful detail for anyone pricing imported inflation. The MPR explicitly assumes oil falls to US$75 by mid-2027 from current elevated prices; the Bank is publishing that trajectory rather than hiding behind a wider band.

3. The growth outlook is essentially unchanged. The April MPR keeps real GDP at 1.2% in 2026, rising to 1.6% in 2027 and 1.7% in 2028. Higher oil prices help Canada on the income side because we are a net exporter — that partially offsets the squeeze on consumers paying more at the pump. Tariffs and trade-policy uncertainty continue to weigh on exports and business investment.

Layer on a labour market with unemployment in the 6.5%–7% range and population growth that has slowed materially (which the Bank cited as a drag on housing activity in Q4 2025), and the case for sitting still while the energy shock works through is the cleaner read on the data.

What it means for mortgage rates

Variable rates do not move today. Prime stays at 4.45% at the major Canadian lenders. A $700,000 variable-rate mortgage at P+0.50% remains at 4.95% — same payment, same rate, same amortization as April 28. HELOC rates hold too.

Fixed rates move with bond yields, not the overnight rate. The five-year Government of Canada yield has drifted higher since January as bond markets priced the energy-led inflation bump. Best-in-market five-year insured fixed sits in the 4.05%–4.25% range. Three-year insured runs slightly lower and is the more popular choice in 2026 — it lets renewers re-price into what economists expect to be a lower-rate environment in 2027–2028 without taking variable risk now.

What matters from here: whether the April CPI print on May 20 comes in near the Bank's ~3% expectation, or surprises higher. A clean energy-only print keeps the "look-through" framing intact and bond yields pinned. A core surprise — services, food, durables — would put the Bank's June 4 decision on the table in a different shape.

What it means for the GTA spring market

The market is not going to whipsaw on a hold that was 92% priced in. What it does is preserve the cautious recovery we already had:

- March 2026 GTA sales rose 1.7% year-over-year — the first positive print in six months. Average price held tight around $1.02 million. New listings ran cool. None of that flips on today's announcement.

- The Carney–Ford HST relief on new construction remains the single biggest tailwind for buyers in pre-construction-heavy submarkets (Milton, Oakville North, Brampton NW, East Gwillimbury). The new-build math has shifted in ways resale math has not.

- The Bank explicitly flagged that slow population growth is now part of why housing activity is soft — a structural point that a single rate cut would not have changed.

For sharply priced inventory, 7–14 day timelines remain the norm. Overpriced listings are still sitting. List timing in late April–early May still looks like a reasonable window: ahead of the new-build pull-through that HST relief is creating, and before the May 6 TRREB release reframes spring narrative either way.

What it means if you're renewing

Roughly 1.2 million Canadian mortgages renew in 2026, and most of the cohort signed at sub-2% rates in 2020–2021. If your renewal lands between now and August:

- Variable hold: today is a non-event for you. Run the spread vs. a 3-year fixed at today's quote — it has narrowed materially since January.

- Fixed renewal: five-year insured around 4.05%–4.25%; three-year insured slightly lower. The 3-year is the consensus pick this cycle.

- Stress test still applies on lender switches: the uninsured stress test requires qualifying at the contract rate plus 2% (or 5.25%, whichever is higher). Straight-switch insured renewals stay exempt under OSFI's 2024 update.

Get a written quote this week. Most lenders hold for 90–120 days; the rate you secure today survives the June 4 decision either way.

Watchlist for the next 30 days

- May 6: TRREB April 2026 Market Watch — tells us whether the March uptick is a trend or a one-month pop.

- May 20: Statistics Canada April CPI — the single biggest input to the June 4 BoC decision. The Bank has guided ~3% headline.

- June 4: Next BoC policy decision (no MPR — the next full report lands in July).

- Summer onwards: Iran/oil trajectory. The April MPR's assumed path back to US$75 is what the Bank will be tracking against.

A separate post-CPI piece will follow on May 20 once we see whether April inflation lands where the Bank expects.

Questions about how today's decision affects your specific purchase, sale, or renewal? Reach out — happy to walk the numbers.

Sources

- Bank of Canada — Policy rate announcement, April 29, 2026

- Bank of Canada — Opening statement, April 29, 2026

- Bank of Canada — Monetary Policy Report, April 2026

- Statistics Canada — Consumer Price Index, March 2026

- TRREB — March 2026 Market Watch

- OSFI — Minimum qualifying rate for uninsured mortgages

Frequently asked questions

No. The Bank held its target for the overnight rate at 2.25% — the fourth consecutive hold and six straight months at this level. The Bank Rate is 2.5% and the deposit rate is 2.20%. OIS markets had priced roughly an 8% probability of a cut going into the meeting.

The Iran war pushed oil and gasoline higher, lifting March headline CPI to 2.4% with April expected near 3%. The Bank chose to look through the energy shock rather than cut into rising headline inflation. Underlying core inflation is still near 2%, which preserves room to ease later if the shock fades.

The April Monetary Policy Report projects real GDP growth of 1.2% in 2026, 1.6% in 2027, and 1.7% in 2028 — little changed from January. After a Q4 2025 contraction, growth is forecast to have resumed in early 2026. Unemployment is in the 6.5%–7% range, with job losses concentrated in tariff-exposed sectors.

No change. Variable rates and HELOCs are priced off prime, which sits at 4.45% at the major Canadian lenders (BoC overnight + 2.20%). With the Bank on hold, prime does not move, and your variable payment, rate, and amortization stay where they were on April 28.

Fixed rates track 5-year Government of Canada bond yields, not the overnight rate. Yields are modestly higher than January as energy-driven inflation expectations have firmed. Best-in-market 5-year insured fixed rates remain in the 4.05%–4.25% band. Get a written quote — most lenders hold for 90–120 days.

June 4, 2026. Between now and then, the two biggest data points are the May 6 TRREB April Market Watch and the May 20 Statistics Canada April CPI release. April CPI is expected to print near 3% on energy pass-through; the Bank has signalled it will look through the headline lift unless expectations slip.