April 27, 2026 · The Couple Estates

BoC April 29 Rate Preview: What GTA Buyers and Renewers Should Watch

The Bank of Canada decides April 29, 2026 with rates at 2.25%. Markets price ~8% odds of a cut. Here's what's at stake for GTA buyers and renewers.

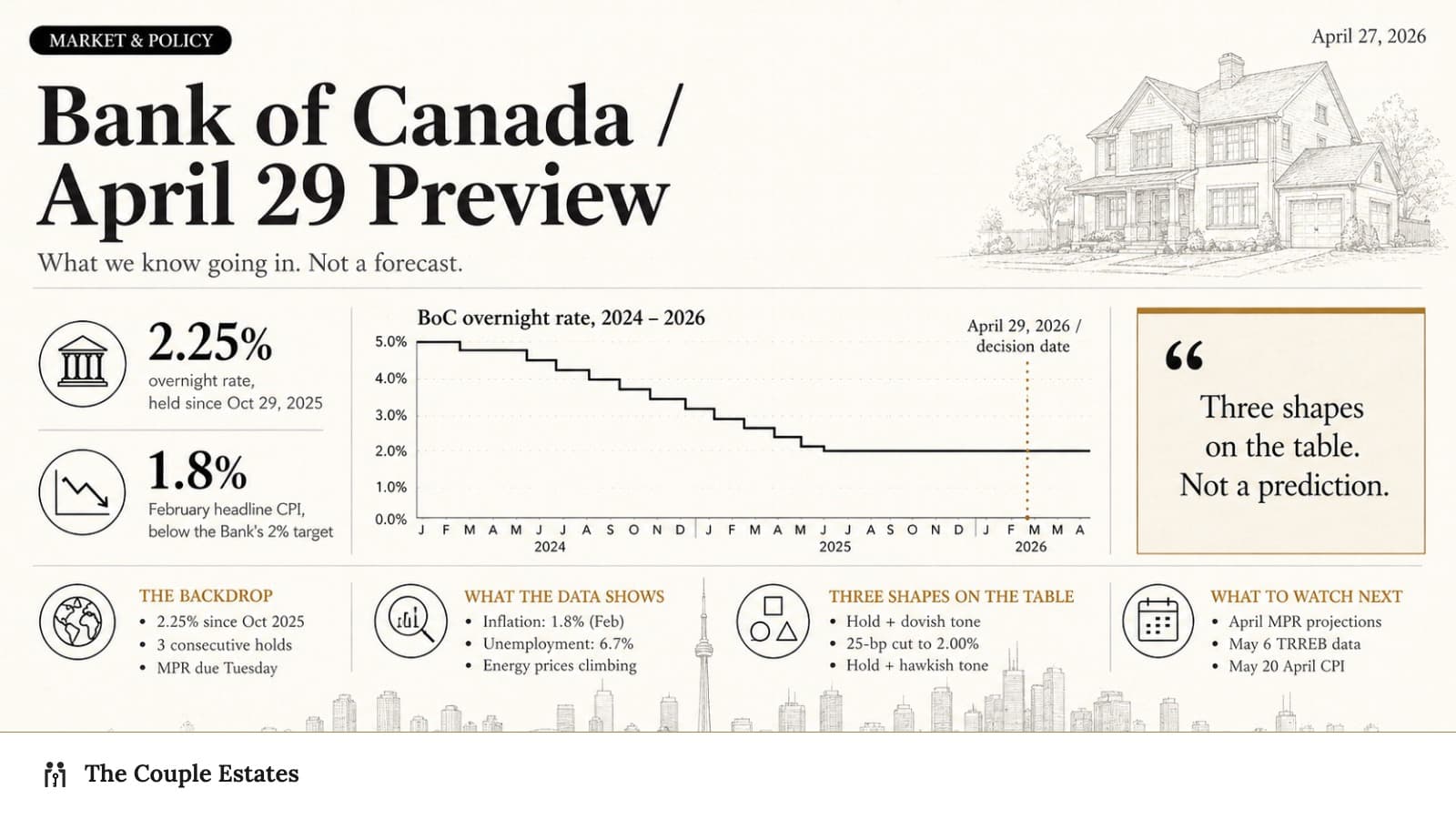

The Bank of Canada decides on Tuesday, April 29 — the fourth rate decision of 2026, and the first one paired with an updated Monetary Policy Report since January. The policy rate has been parked at 2.25% since October 29, 2025. Three holds in a row form the backdrop heading into Tuesday — what the Bank does next is its call to make.

This piece is not a prediction. It walks through what the Bank is looking at, what bond markets are currently pricing, and how each plausible outcome would land for someone buying, selling, or renewing a mortgage in the GTA this spring. The post-decision recap will follow on April 29.

The bottom line

- Policy rate: 2.25% — held since October 29, 2025. Three consecutive holds (December, January, March).

- What's priced in (as of April 27): OIS markets imply roughly an 8% probability of a 25-bp cut on April 29 — heavier weight on a hold than a move. Pricing can shift before Tuesday.

- The split mandate: February inflation cooled to 1.8%, but unemployment is up to 6.7% and energy prices are climbing on Iran. The Bank is balancing a labour-market drag against energy-led inflation risk.

- What it could mean: On a hold, variable-rate holders see no immediate change. On a 25-bp cut, prime would adjust within 1–2 business days. Fixed-rate quotes typically move ahead of decisions, so the day-of impact tends to be small.

- What to watch: the MPR's revised inflation and unemployment paths, and any change in Governor Macklem's tone on the trajectory of US tariff pass-through.

Where the policy rate sits going into Tuesday

| Decision date | Rate | Move |

|---|---|---|

| March 18, 2026 | 2.25% | Hold |

| January 28, 2026 | 2.25% | Hold |

| December 10, 2025 | 2.25% | Hold |

| October 29, 2025 | 2.25% | -25 bp |

| September 17, 2025 | 2.50% | -25 bp |

Six months at 2.25% is the longest pause since the 2022–23 tightening cycle. The full context for the March 18 hold — including the Bank's reasoning and the renewer playbook that came out of it — still applies, with two changes since.

What's changed since March 18

Two things have moved in opposite directions over the past six weeks.

1. February CPI confirmed the disinflation story. Headline inflation came in at 1.8% — below the Bank's 2% target and the lowest print since late 2024. Core measures (trim and median) are also clustered near 2%. On its own, that is a green light to cut.

2. Energy is pulling the other way. The conflict in Iran has pushed Brent crude above $90, and Canadian gasoline prices have followed. The Bank flagged this directly in its March statement, telling markets to expect "a temporary lift to headline inflation from energy prices in the coming months." That is exactly the kind of supply-side shock the Bank prefers to look through — but only if expectations stay anchored.

Layer in unemployment at 6.7% (February), softer Q4 GDP, and the cumulative drag from US tariffs, and the Bank's mandate looks genuinely split. Cutting on top of energy-driven price pressure carries one risk; sitting through continued labour-market softness carries another. Both are defensible reads of the data. Markets are currently leaning toward a hold — but that is market pricing, not a forecast we are making.

What the OIS market is actually telling us

As of April 27, overnight index swaps imply roughly an 8% probability of a 25-bp cut on April 29. By the July 30 meeting, the implied cumulative probability of at least one cut sits near 35%. By October, around 55%.

In plain English: bond traders are placing more weight on a summer cut than a Tuesday move, while leaving room for either outcome. The five-year Government of Canada bond yield is sitting near 2.85%, and fixed mortgage rates have drifted down by 5–10 bp over the past two weeks as that pricing has settled. None of this prevents the Bank from doing something different.

Three scenarios that are on the table

These are plausible shapes for Tuesday's announcement — not ranked by probability, because the Bank's decision (and the wording of the statement) is genuinely the Bank's call. Each scenario has happened in past cycles when the data setup looked similar to today's.

Scenario A — Hold with a dovish-leaning statement. Rate stays at 2.25%. Statement acknowledges the energy-driven inflation bump, leans on labour-market softness, and keeps the door open to later cuts. Variable-rate borrowers see no change. Fixed yields edge slightly lower; locked rate quotes typically move very little day-of.

Scenario B — 25-bp cut. Rate moves to 2.00%. Prime would adjust within 1–2 business days from 4.45% to 4.20%. A $700,000 variable-rate mortgage at P+0.50% would see its rate move from 4.95% to 4.70% — roughly $90 per month in payment relief. Fixed quotes typically have a lot of this priced in already.

Scenario C — Hold with a hawkish-leaning statement. Rate stays, but the statement re-emphasises inflation risks and pushes back on near-term cut expectations. Bond yields could rise 5–10 bp. Fixed-rate quotes nudge up. This is the shape that would surprise markets the most given current pricing.

What this could mean if you are buying right now

Spring activity is already off the floor. March 2026 GTA sales rose 1.7% year-over-year — the first positive print in six months — and the average price stabilised in a tight band around $1.02 million. Most of that is in motion regardless of which way Tuesday lands.

If you are pre-approved at March rates, your rate hold is typically good for 90–120 days at most lenders; refreshing it next week is sensible either way. One of the larger tailwinds for buyers this spring sits outside the BoC's control: the Carney–Ford HST relief on new construction. The new-build math has shifted in ways it had not for years; resale math is roughly unchanged.

Waiting specifically for "the cut" before acting on a well-priced listing carries its own risk. In past easing cycles, the first few cuts have tended to draw more buyers off the sidelines, which historically tightens conditions on similar inventory. Past pattern, not a guarantee for this cycle.

What this could mean if you are selling

A single rate decision rarely moves showings or offers in the same week. List timing in April–early May still looks like a reasonable window ahead of the new-build pull-through that the HST relief is creating in pre-construction-heavy submarkets (Milton, Oakville North, Brampton NW, East Gwillimbury).

Historically, when a cut has surprised markets, showing volume has tended to respond after a 1–2 week lag. Pricing remains the lever in either direction. Sharply priced listings are still selling in 7–14 days; overpriced inventory is still sitting.

What this could mean if you are renewing

Roughly 1.2 million Canadian mortgages renew in 2026 — many of them at a rate higher than the original. If your renewal lands between now and August:

- Variable-rate hold: A cut helps. A hold leaves you where you are. Either way, run the spread vs. a 3-year fixed at today's quote.

- Fixed-rate renewal: Five-year fixed insured rates sit around 4.05–4.20% with most lenders. Three-year fixed runs slightly lower. The 3-year is the more popular choice in 2026 because it lets you re-price into the rate cycle's likely 2027 trough.

- Stress test still applies: Switching lenders re-triggers the uninsured mortgage stress test — qualify at the contract rate plus 2% or 5.25%, whichever is higher.

Get your renewal quote in writing this week. Most lenders will hold the rate for 30–120 days; the quote you secure today survives Tuesday's decision either way.

Watchlist for the next 30 days

- Tuesday, April 29: BoC decision and Monetary Policy Report.

- April 30: RBC, BMO, TD, Scotiabank, CIBC each publish their reaction notes — read at least two before adjusting your view.

- May 6: TRREB April 2026 Market Watch. Tells us whether the March uptick is a trend or a one-month pop.

- May 20: Statistics Canada April CPI. The single biggest input to the BoC's June 4 decision.

A separate post-decision article will follow on the afternoon of April 29 with what the Bank actually did, the language used in the statement, and the revised numbers in the MPR. The market & policy hub is where it will land.

Questions about how either outcome could affect your specific purchase, sale, or renewal? Reach out — happy to walk the numbers either way.

Post-decision recap to follow on 2026-04-29.

Sources

- Bank of Canada — Policy interest rate

- Bank of Canada — Schedule of interest rate announcements 2026

- Bank of Canada — March 18, 2026 policy rate announcement

- Statistics Canada — Consumer Price Index, February 2026

- Statistics Canada — Labour Force Survey, February 2026

- TRREB — March 2026 Market Watch

Frequently asked questions

The overnight rate is 2.25%, where it has been since the October 29, 2025 cut. The Bank held at this level on December 10, 2025, January 28, 2026, and March 18, 2026 — three consecutive holds going into the April 29 decision.

No one outside the Bank knows. As of April 27, 2026, OIS markets imply roughly an 8% probability of a 25-bp cut at the April 29 meeting — pricing, not a forecast. Most published bank-economist commentary has leaned toward a hold, with summer cited as a more plausible cut window if inflation continues cooling.

Variable-rate mortgages and HELOCs move with prime within 1–2 business days of a BoC change. A 25-bp cut shaves about $13 per month on every $100,000 of variable-rate mortgage balance at current pricing — meaningful, but not market-moving.

Fixed mortgage rates are priced off Government of Canada bond yields, not the overnight rate. Bond markets already price the expected outcome days in advance, so locking right before the announcement rarely changes your offered rate by more than a basis point or two.

Only at the margin. March 2026 GTA sales rose 1.7% year-over-year — the first positive print in six months — but the move came alongside softer prices and lower new listings rather than an imminent rate change. In past cycles, sustained recovery has typically required some combination of lower rates and stronger buyer confidence.