January 21, 2026 · The Couple Estates

The GTA Condo Collapse: 1,599 New Sales in 2025 — A 35-Year Low — And What It Means for Buyers in 2026

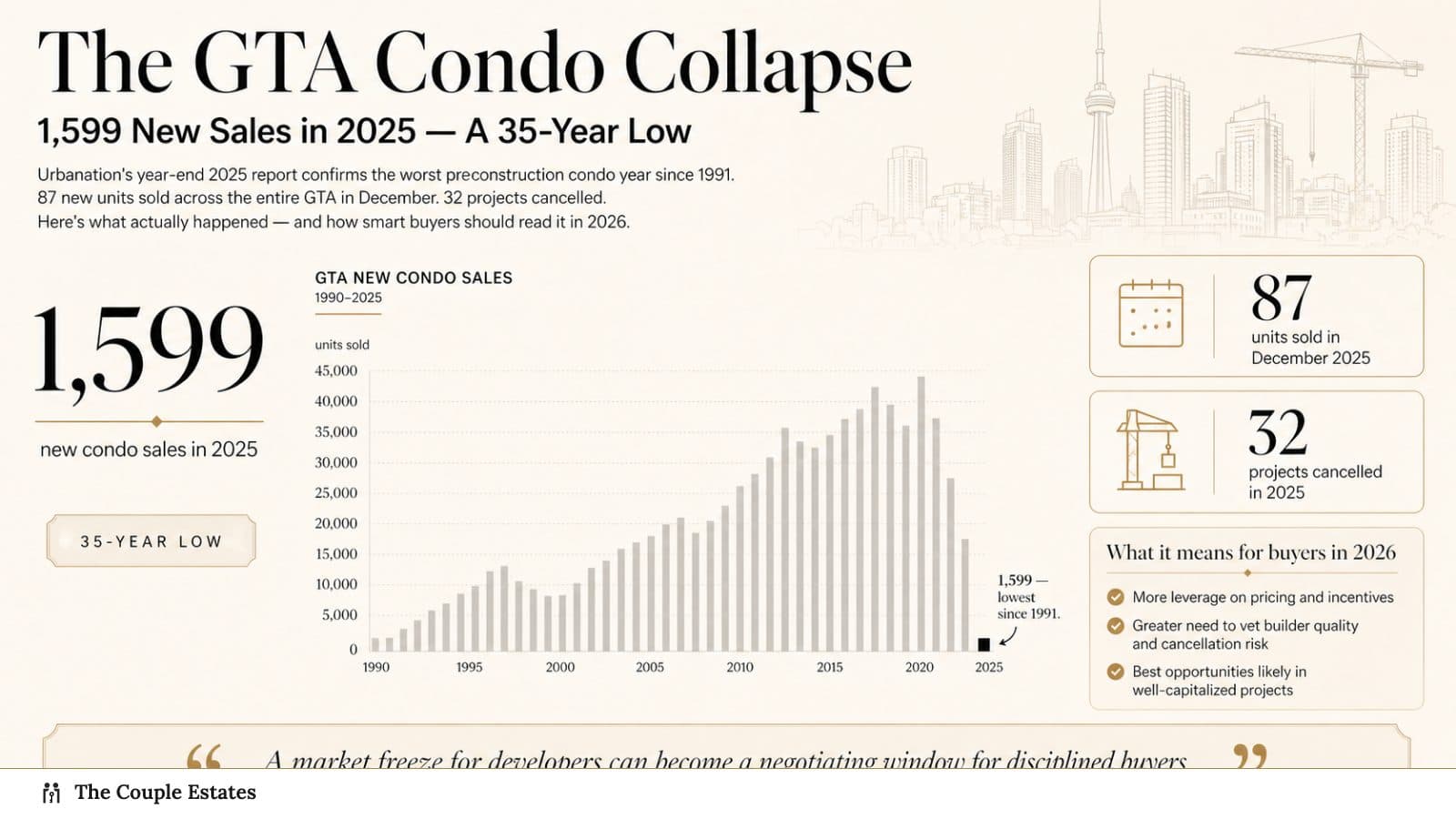

Urbanation's year-end 2025 report confirms the worst pre-construction condo year since 1991. 87 new units sold across the entire GTA in December. 32 projects cancelled. Here's what actually happened and how smart buyers should read it.

Urbanation released its year-end 2025 report this morning, and the numbers are worse than most industry people were whispering at the end of Q4.

1,599 new condominium sales across the entire GTHA in 2025. That's lower than every year since 1991 — lower than the 2008 financial crisis, lower than the pandemic shutdown, lower than any recession in living memory. For context, the 2021 peak was 31,061 new condo sales. We are down 95% in four years.

If you're a pre-construction investor, a buyer waiting for "the bottom," or just someone trying to make sense of what your downtown condo is now worth, here's what the data actually says — and how to read it.

The numbers

| Metric | 2021 peak | 2024 | 2025 |

|---|---|---|---|

| New condo sales (GTHA) | 31,061 | ~4,000 | 1,599 |

| December monthly sales | ~2,400 | ~400 | 87 |

| Projects cancelled / receivership (cumulative since Jan 2024) | 0 | ~10 | 32 projects / 6,981 units |

| Additional projects on hold or in receivership | — | — | 20 projects / 4,187 units |

| Projects cancelled in 2025 alone | — | — | 28 projects / 7,200+ units |

87 units in December. Across 16 million people. That is not a correction — it is a market that has genuinely stopped functioning at the pre-construction layer.

Annual new condominium apartment sales in the GTHA. 2025 closed at 1,599 units — the lowest annual total since 1991. Source: Urbanation.

Annual new condominium apartment sales in the GTHA. 2025 closed at 1,599 units — the lowest annual total since 1991. Source: Urbanation.

What actually broke

Four things stacked on top of each other.

1. The investor exit. At the peak, investors represented more than half of pre-construction buyers. They were underwriting deals on the assumption of 5% annual appreciation and 2% mortgage rates. When appreciation turned negative and rates tripled, the math flipped from "pay a small monthly gap for five years and profit on assignment" to "cover a $1,200 monthly negative cash flow indefinitely." Investors stopped buying. Then some stopped closing.

2. The financing wall. Builders need ~70% pre-sales to secure construction financing. With sales collapsing, financing stalled. Projects that launched in 2022–2023 and failed to hit pre-sale thresholds started rolling into receivership in 2024 — 32 projects and nearly 7,000 units are now cancelled or functionally cancelled since the start of 2024.

3. The inventory overhang. Units that launched in 2020–2022 are now completing — and a chunk of those completions arrive in the hands of buyers who no longer want them or can't afford to close. Completed-but-unsold inventory is at a record high. Every one of those units competes with resale listings and drags prices down further.

4. Affordability. Even with prices off 20%+ from peak, a 500 sq ft downtown Toronto one-bedroom at $620,000 requires roughly a $125,000 household income, a $31,000 down payment, and about $4,000/month of all-in carrying cost. That is a vanishing end-user buyer in a city where median rents are $2,300.

Where pockets are holding up — and where they're not

It is not all uniform. The Urbanation data and TRREB's MLS HPI show clear divergence:

- Vaughan Metropolitan Centre (VMC): Prices up 8.6% YoY to ~$655,442. Reason: reduced municipal DCs under Bill 17, genuine transit access, end-user demand.

- Mississauga Square One / Hurontario corridor: Prices down ~6% YoY. Investor-heavy, heavy new supply from 2022 completions.

- Downtown Toronto (C01): Prices down ~9–11% YoY. The deepest correction. Most completions, most investor flight.

- Etobicoke / The Queensway: Down ~5% YoY. Holding up better than downtown on end-user demand from young families priced out of freeholds.

- North York (Yonge / Finch): Down ~7% YoY. Decent end-user demand, but hit by pre-construction completions in 2025.

Location still matters. So does building quality, maintenance fee structure, and who the original developer was.

What this means if you're a buyer right now

Three honest takes, depending on who you are.

If you're an end-user buying to live in: This is the best buyer's market in GTA condos since 2009. You have time, selection, and negotiation leverage. Floor plans that were getting 10 offers in 2022 are sitting for 60+ days. Target completed, 2020-and-newer buildings with reasonable maintenance fees (under $0.80/sq ft is a sane benchmark). Avoid buying on assignment unless your lawyer has reviewed the deposit structure and builder covenants.

If you're an investor: Cap rates on new-build GTA condos are negative at list prices with today's rates. They will not pencil until either (a) prices fall another 10–15% or (b) rates drop meaningfully. If you must buy, focus on resale in low-fee buildings with strong rental demand — pre-construction is where leveraged investors go to die right now.

If you're holding a pre-construction assignment you need out of: Talk to your lawyer before your broker. There are paths — deposit recovery, builder negotiation, even pursuing the builder's marketing assurances in some cases — but the first mistake most people make is trying to "solve" this through aggressive repricing of the assignment. The assignment market is effectively frozen. A lawyer can often get you more than the market can.

What this means if you're selling a condo

Price to the comp that actually sold in the last 60 days, not to your neighbour's 2022 listing. Stage. Clear pet smells (seriously — this is the #1 killer of condo showings). Consider a 2–4 week price improvement cadence rather than a single chase-the-market drop.

The buyers are there. They are just smaller in number and much more selective. Properties priced correctly are selling within 30 days. Overpriced listings are sitting for 90+ and accumulating stink.

Browse current GTA condo listings or talk to us about pricing your unit if you're thinking of listing this spring.

Where this goes from here

The industry consensus — and I think it's right — is that new condo starts in the GTHA will fall close to zero in 2026 and 2027. Urbanation is flagging the possibility of "no new condo completions" in the GTHA by the end of the decade, because projects that would have been selling and pre-selling today simply aren't.

That matters because it is the seed of the next supply crunch. The GTA adds roughly 100,000 people per year. If pre-construction goes to zero for two to three years, we will be staring at the same affordability crisis in 2029 — just with fewer units than we thought.

The near-term is a buyer's market. The medium-term is almost certainly a seller's market again. Which end of that cycle you want to be on depends on your timeline.

If you want to go deeper on a specific building, a specific pocket, or what your unit is actually worth in today's market, reach out — happy to pull the recent comps and walk through it.

Sources

- Urbanation — Slowest Condo Market in Over 30 Years

- Urbanation — Condo Project Cancellations Hit Record High

- Urbanation — "No New Condo Completions" by Decade's End

- RBC Economics — Navigating Toronto's frozen pre-construction condo market

- Deeded — Toronto Condo Meltdown: What's Really Going On

- Real Estate Magazine — Worst pre-construction condo market ever